No Money DownAuto Loans

Exploring $0 down options for bad credit? Here's what's really possible with trade-ins, co-signers, and specialized programs.

Looking for no money down car loans? We'll show you the honest path. True zero down auto financing is rare with bad credit, but there are smart ways to minimize out-of-pocket costs.

Let's Be Honest About "Zero Down" for Bad Credit

While the term "no money down" gets searched frequently, the reality for subprime borrowers is more nuanced. True $0 out-of-pocket with bad credit is extremely rare. Here's what "zero down" typically means in practice:

- Trade-In as Down Payment: You use your current vehicle's equity instead of cash (most common "zero down" scenario)

- Co-Signer with Better Credit: Someone with stronger credit co-signs, reducing lender risk and eliminating down payment need

- Very Strong Income (Rare): If you earn $4,000+ monthly with 2+ years job stability, some lenders may waive down payment

- Dealer Assistance Programs: Some dealers offer "first month's payment as down" or roll fees into the loan

Our Recommendation: If you can save even $500-$1,000, you'll get better approval odds and lower interest rates. But if you truly have zero cash and need a car for work, the options above are how dealers make it work. We'll be honest about what's possible for YOUR specific situation. Learn more about bad credit auto loans and what affects your approval odds.

How No Money Down Loans Work

Our network of dealers can help you explore zero down payment options. Here's how the process works.

Complete Pre-Qualification Form

Fill out our quick 3-minute online pre-qualification form. No money down options are evaluated based on your income and credit profile.

Dealer Reviews Your Options

Our network of dealers reviews your pre-qualification to determine if you qualify for reduced/zero down programs (often requiring trade-in equity, co-signer, or higher income).

Drive Home Today

Visit the dealership, finalize your loan terms, and drive home in your new vehicle - all without a down payment.

Benefits of No Money Down Financing

Zero down payment auto loans offer several advantages for buyers who need a vehicle but don't have cash on hand.

Keep Your Cash

Preserve your savings for emergencies, other expenses, or investments instead of using it all for a down payment.

Build Credit History

Make consistent monthly payments to improve your credit score over time, helping with future financing needs. Use our loan calculator to estimate your payment.

Get a Car Immediately

Don't wait months to save for a down payment. Get the transportation you need for work and daily life right now.

Lower Barrier to Entry

Makes car ownership accessible even if you haven't had time to save thousands of dollars for a traditional down payment.

Flexible Terms

Work with dealers who offer various loan terms and payment options tailored to your budget and financial situation.

All Credit Welcome

Bad credit, no credit, bankruptcy, or repossession? We work with dealers who specialize in all credit situations.

Qualification Requirements

Here's what you typically need to qualify for a no money down auto loan

Basic Requirements

- Stable Income: Proof of consistent employment or income (paystubs, bank statements)

- Valid ID: Government-issued driver's license or state ID

- Proof of Residence: Utility bill, lease agreement, or mortgage statement

- Insurance: Ability to obtain full coverage auto insurance

- Age: Must be 18 years or older (19 in some states)

Important Considerations

- Higher Interest Rates: Zero down loans may have higher APRs compared to traditional financing

- Credit Impact: Your credit score and history will affect loan terms and rates

- Income Verification: Lenders need to ensure you can afford monthly payments

- Loan-to-Value: You may start with negative equity if the car depreciates

- Vehicle Selection: Some dealers limit zero down options to specific inventory

Don't Meet All Requirements?

Pre-qualify anyway! Our dealer network specializes in finding solutions for unique situations. Even if you don't meet all traditional requirements, you may still qualify for financing. Every pre-qualification is reviewed individually, and we work hard to find a path to approval.

When Does $0 Down Make Sense?

Zero down financing isn't right for everyone. Here's when it works best and when you might want to reconsider.

When Zero Down Works Well

- Emergency Transportation Need: You need a car immediately for a new job and can't wait to save

- Strong Stable Income: You earn $3,000+ monthly and can comfortably afford the higher payment

- Credit Building Focus: You prioritize establishing payment history over minimizing interest costs

- Cash Reserved for Emergencies: You have savings but wisely want to keep them for unexpected expenses

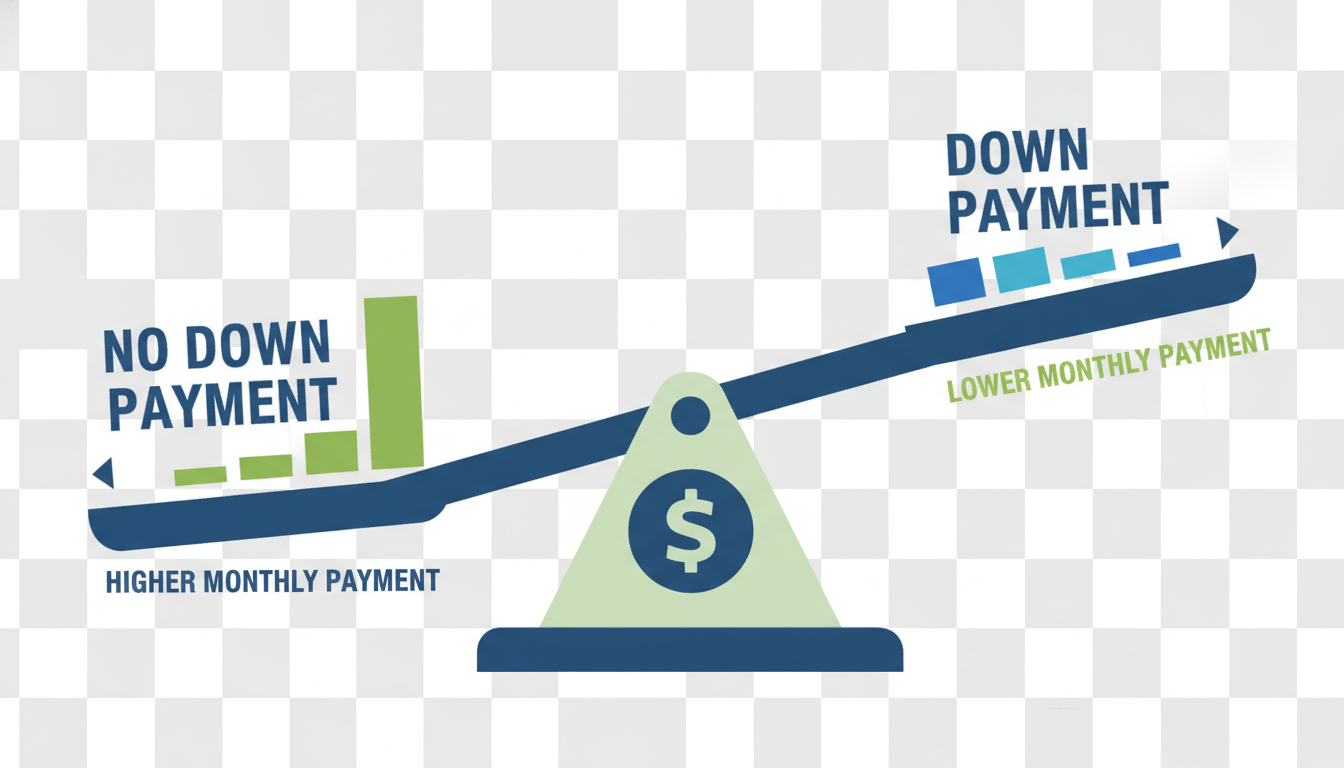

Consider a Down Payment If...

- You Have Deep Subprime Credit (300-500): A $1,000-$2,000 down payment can dramatically improve approval odds and rates

- Monthly Budget is Tight: Even $500 down can lower your payment by $20-$30/month

- Buying a Higher-Priced Vehicle: Down payments reduce the risk of negative equity if the car depreciates

- You Want the Lowest Interest Rate: Lenders reward down payments with better APRs (can save 2-4% on your rate)

Common Questions

Everything you need to know about no money down auto loans

Can I really get a car with no money down?

Yes! Many dealers offer zero down payment programs, especially for buyers with stable income. While requirements vary by lender, our network specializes in helping people secure financing without requiring thousands upfront for a down payment.

Will my credit affect my ability to get zero down financing?

Your credit does play a role in loan terms and interest rates, but we work with dealers who approve all credit types for no money down loans. Bad credit, no credit, bankruptcy, and repossession situations are all considered. Your income and employment stability matter most.

Are monthly payments higher with no money down?

Since you're financing the full purchase price, monthly payments may be slightly higher than if you made a down payment. However, you preserve your cash for other needs. Our dealers offer flexible terms to keep payments manageable within your budget.

How long does the approval process take?

Most applications receive a response within 2-4 hours during business hours. Once approved, you can typically visit the dealership the same day or next business day to finalize paperwork and drive home in your vehicle.

Explore More Financing Options

Looking for other ways to get approved? Check out our specialized financing programs.