Bad Credit Auto Loans?We Know Dealers Who Say Yes.

500 credit score? Bankruptcy? Repo? Collections? We've matched over 1 million people with dealers who specialize in credit challenges. Your situation isn't new to us.

If you're searching for bad credit auto loans or even a 500 credit score car loan, you're in the right place. We focus on practical approvals—not hype—and we guide you toward realistic payments.

Many lenders still say yes to bad credit car loans when income is steady and the vehicle fits the budget. We match you with those dealers so you can get back on the road.

Why Bad Credit Auto Loans Matter

Bad credit car loans exist because life happens—medical bills, job changes, or repossessions. You're not alone, and you're not judged here.

Medical Expenses

Unexpected medical bills can quickly overwhelm even the most prepared households. We look at your recovery, not just the debt.

Job Loss

Employment gaps happen. If you have income now, we can help you get back on the road to stability.

Divorce

Separation often brings credit challenges. We're here to help you move forward with dignity and independence.

Bankruptcy

Chapter 7 or 13? We specialize in post-bankruptcy auto loans that serve as your first step to rebuilding.

Past Mistakes

Made poor financial decisions years ago? Everyone deserves a chance to prove they've grown.

No Credit History

New to the US or just starting out? We help you establish a positive credit history from day one.

Understanding Bad Credit Car Loans: A Complete Guide

What is a Bad Credit Car Loan?

A bad credit car loan (often called specialized auto financing) is a specialized type of financing designed for drivers with credit scores below 660. Unlike traditional auto loans from big banks that rely heavily on a high credit score for approval, these loans focus on your complete financial picture.

Specialized lenders understand that a three-digit number doesn't tell your whole story. They look at "stability factors"—like your employment history, income level, and residence stability—to determine your ability to repay the loan. This approach allows people with past bankruptcies, repossessions, or simply no credit history to secure essential transportation for work and family needs.

Credit Score Ranges Explained

Knowing where you stand is the first step to getting a fair deal. Auto lenders typically categorize credit scores into specific "tiers" that determine your interest rate and approval odds.

| Credit Tier | Score Range | What to Expect | Typical APR Est.* |

|---|---|---|---|

| Credit Challenged | 300 – 500 | Approval is possible but requires proof of income. Expect higher rates and down payment requirements. Focus on affordable reliable cars. | 18% – 24%+ |

| Specialize Lenders | 501 – 600 | Better approval odds. You may have more vehicle choices. Lenders will still verify income and employment strictly. | 14% – 20% |

| Near Prime | 601 – 660 | The "transition" zone. You are close to standard rates. Shopping around can save you significant money here. | 10% – 16% |

| Prime | 661+ | Traditional financing territory. You likely qualify for standard bank rates and manufacturer incentives. | < 10% |

*Rates are estimates for educational purposes only and vary based on the lender and current economic conditions.

How Bad Credit Auto Loans Work

The process for specialized auto financing is slightly different from a standard car purchase. Instead of finding a car first and then figuring out financing, the process usually works best in reverse:

- Pre-Qualification: You submit basic information to see what you might qualify for without impacting your credit score.

- Lender Matching: Dealers work with a network of specialized lenders who compete for your business.

- Budget Determination: The lender determines a maximum monthly payment you can afford based on your income (not just your credit score).

- Vehicle Selection: You choose a car that fits within that approved budget.

Loan terms typically range from 24 to 72 months. While longer loans lower your monthly payment, they increase the total interest you pay. We encourage keeping the term as short as comfortably possible to build equity faster. Use our auto loan calculator to estimate your monthly payment based on your credit situation.

Want to understand our complete approval process? See how it works in 3 simple steps.

Key Factors That Affect Your Loan Rate

While your credit history matters, lenders consider multiple factors when evaluating your application. Understanding these helps you improve your approval odds.

Credit Score

Your score shows lenders your history, but it's not the only factor. Dealers can work with scores from 300-850, focusing on your current situation and income stability.

Down Payment

Even a modest down payment of $500-$1,000 significantly improves approval odds and lowers your monthly payment. It shows lenders your commitment and reduces their risk.

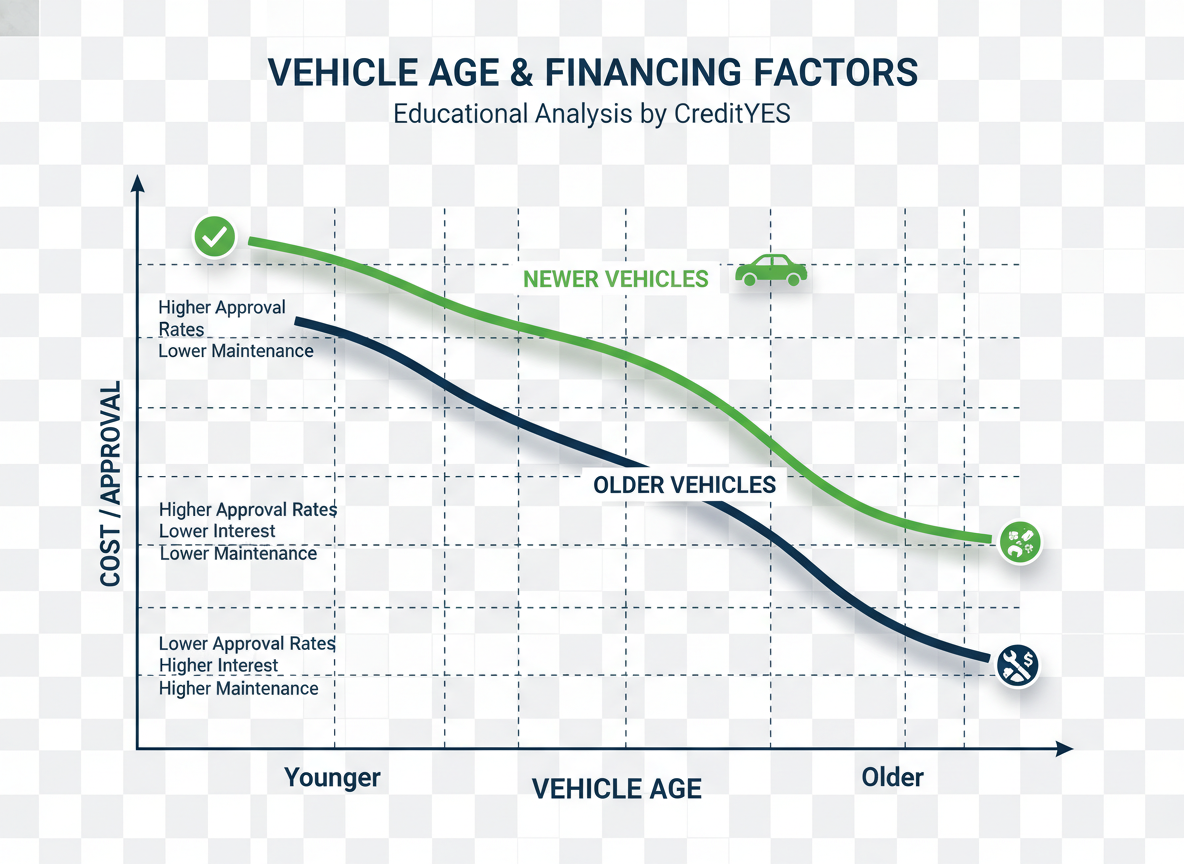

Vehicle Age

Newer vehicles typically qualify for better rates and longer terms. Older vehicles may have higher rates but lower purchase prices, which can work in your favor with the right dealer.

How Car Approval Pro Makes It Possible

We've built our reputation on second chances and treating people with respect.

Trusted Dealer Network

We've spent over 30 years building relationships with dealerships in your area that specialize in credit-challenged situations. These dealers have the lender relationships and subprime expertise to help people that traditional dealerships turn away.

Dealers Who Look Beyond The Score

Our partner dealerships consider your current situation, not just past mistakes. Steady income, job stability, and reasonable down payment can often outweigh a poor credit score. They look at the complete picture of your financial life.

A Path to Rebuild Credit

Every on-time payment you make gets reported to major credit bureaus. Your auto loan becomes a tool to rebuild your credit score. Many customers who work with our partner dealerships see significant improvements within 12-18 months.

Success Stories: Real People, Real Approvals

We believe everyone deserves a second chance. Here are realistic examples of how subprime auto financing helps people get back on the road.

The "Fresh Start" After Bankruptcy

Meet John: A warehouse manager with a 520 credit score

Situation: John filed for Chapter 7 bankruptcy due to medical bills. It was discharged 18 months ago. He earns $35,000 annually but was rejected by his bank.

The Approval: He was matched with a dealer specializing in post-bankruptcy lending.

The Deal: $15,000 loan for a used sedan | 17% APR | 60-month term | $370/month.

The Outcome: John put down $1,500. He now has a reliable car to get to work. By making on-time payments for a year, his credit score improved to 620, qualifying him for a lower rate on his next car.

Recovering from Repossession

Meet Maria: A nursing assistant with a 480 credit score

Situation: Maria lost her job two years ago, leading to a voluntary repossession. She is now employed steadily, earning $2,800 a month.

The Approval: Lenders looked at her 12 months of steady job history rather than just the past repo.

The Deal: $12,000 loan for a compact SUV | 21% APR | 48-month term | $375/month.

The Outcome: Maria saved a $2,000 down payment, which convinced the lender of her commitment. After 18 months of perfect payments, she refinanced the loan to a 12% rate, saving her hundreds of dollars.

First-Time Buyer with No History

Meet Alex: A recent grad with a "Ghost" score (0 credit score)

Situation: Alex has never had a credit card or loan. He earns $32,000/year but has no "trust" built with banks.

The Approval: A "First-Time Buyer" program helped him get approved based solely on his income and a small down payment.

The Outcome: He secured a modest loan for a starter car, effectively building his credit history from scratch.

The Medical Debt Trap

Meet Sarah: A teacher with a 550 score due to collections

Situation: Sarah has great job stability (5 years at the same school) but $5,000 in medical collections tanked her score.

The Approval: The lender excluded medical debt from their "Debt-to-Income" calculation, focusing only on her ability to pay the car loan.

The Outcome: She drove away in a reliable vehicle with a payment that fit her monthly teacher's salary.

Real Stories, Real Success

Thousands of customers have rebuilt their financial lives with Car Approval Pro. From bankruptcy to repossession, we help people find a path to ownership every day.

How to Improve Your Approval Chances

Approval is never guaranteed, but you can significantly stack the odds in your favor. Lenders are looking for signs that you are stable and ready to pay.

1. Stable Income is Key

Lenders value consistency. They want to see that you have had the same job or income source for at least 6 months. If you are self-employed, having 3 months of bank statements ready is crucial. Your income matters more than your credit score in subprime lending.

2. Save for a Down Payment

Money talks. Even a small down payment of $500 to $1,000 sends a powerful signal to lenders. It shows you are committed to the car and reduces the amount the lender has to risk. It also lowers your monthly payment instantly and can improve your interest rate.

3. Consider a Co-Signer

If your credit is in the "Deep Subprime" range, a co-signer with better credit can be a game-changer. Their score can help you get approved for a lower interest rate, saving you thousands over the life of the loan. Make sure both parties understand the responsibility.

4. Be Realistic About Budget

Don't shop for your dream car; shop for the car you need right now. Applying for a vehicle that fits comfortably within 10-15% of your monthly income drastically increases your approval odds and sets you up for long-term success.

5. Gather Documentation Early

Speed up the process by having your "proof" ready. You will typically need your driver's license, two recent pay stubs, a utility bill (proof of residence), and references. Being prepared shows lenders you are organized and serious.

Common Questions

How bad can my credit be and still find a dealer?

Our dealer network works with credit scores as low as 450 and even helps people with recent bankruptcies, repossessions, or no credit history. Your current income and ability to make payments matter more than past mistakes.

Will filling out the form hurt my credit score?

No. Car Approval Pro does not check your credit. We simply collect your information and connect you with a dealer in your area. A credit check only happens when you visit the dealership and complete the financing process with them.

What interest rate should I expect?

Interest rates depend on your specific situation and which lender the dealership works with. Bad credit loans typically range from 10-24% APR. While higher than prime rates, this is an investment in rebuilding your credit. Many customers refinance to lower rates after 12-18 months of on-time payments.

What is the minimum credit score for a car loan?

There is no universal minimum score. While traditional banks often require 660+, subprime lenders specialize in helping people with scores between 300 and 600. Income and job stability are often more important than the score itself when working with our dealer network.

How much should I put down on a bad credit car loan?

We recommend aiming for at least 10% of the car's price or $1,000, whichever is less. A down payment reduces your monthly payment and proves to lenders that you are financially invested in the vehicle. However, some dealers do offer $0 down programs for qualified buyers.

Can I get approved with a 500 credit score?

Yes, approval with a 500 score is very common in subprime financing. Lenders will focus heavily on your income, employment history, and "debt-to-income" ratio rather than your past credit mistakes. Many of our customers have scores in the 450-550 range and get approved successfully.

How long does it take to rebuild credit with a car loan?

If you make every payment on time, you may see improvements in your credit score within 6 to 12 months. Auto loans add "installment credit" diversity to your report, which is a positive factor for credit scoring models. Many customers see 50-100 point increases within 18 months.

What documents do I need for a bad credit car loan?

Generally, you will need: (1) Valid Driver's License, (2) Proof of Income (recent pay stubs or bank statements), (3) Proof of Residence (utility bill or lease agreement), (4) Proof of Insurance, and (5) 5-6 Personal References. Having these ready speeds up the approval process significantly.

Can I refinance a bad credit car loan later?

Absolutely. In fact, this is a smart strategy. Many buyers take a higher-rate loan to get the car they need now, make on-time payments for 12-18 months to improve their score, and then refinance into a new loan with a much lower interest rate. This can save thousands in interest.

What's the difference between subprime and deep subprime?

"Subprime" generally refers to scores between 501-600, where borrowers might have one or two major negative marks. "Deep Subprime" (300-500) usually involves multiple active issues or very recent bankruptcy. Deep subprime loans often require larger down payments and have stricter income verification.

Explore More Financing Options

Looking for specific financing solutions? Check out our other programs designed for your situation.

No Money Down Auto Loans

Need a car but don't have cash for a down payment? Learn about $0 down financing options, trade-in strategies, and co-signer programs.

Subprime Auto Financing

Understand how subprime auto financing works, compare lender types, and learn why specialized dealers offer better approval odds.